The future of the housing market in Australia in 2026: Housing market to where?

The Australian property market has continued to be a vital source of household wealth and economic confidence for the country going forward to 2026. Following market momentum created in 2024 and 2025, 2026 is now to be another determining year for buyers and investors in the Australian real estate market, and here they face a supply crunch, affordability issues and changing demand trends.

The new findings of Cotality in their annual report of Decoding 2026 show that 87% of industry participants expect dwelling values to rise appreciate in the year to come, and very few respondents predict a decline in prices. This is indicative of general optimism in the Australian housing market outlook 2026.

Buyer Insight presents a comprehensive property market forecast for 2026 in this article, including the property price and regional trends, as well as the key aspects defining the choice of Australian property investors.

2025 Momentum Carrying into 2026

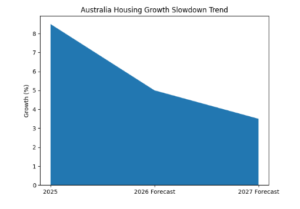

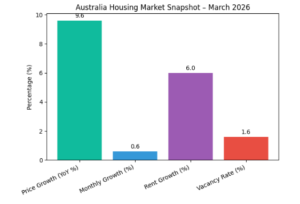

The national dwelling values rose sharply in 2025, with the December Home Value Index by CoreLogic indicating an 8.6% growth in housing values at the national level of about $71,400 to the median home price.

This performance identifies two key sources of Australian housing market growth:

- Unrelenting shortages of housing supply – new construction has not kept up with population growth.

- strong buyer demand – fuelled by migration, employment stability and rental pressure.

These factors contributed towards keeping confidence in the property price outlook Australia, notwithstanding increasing costs of living and the difficulty with borrowing.

National Price Forecasts for 2026

Several industry reports reveal that 2026 will bring additional growth in prices but the rate will differ in different regions and dwelling types.

According to the KPMG Residential Property Market Outlook, national house prices will increase by up to 7.7% in the year 2026, and unit prices will also grow by an average of 7.1%.

This is a balanced housing market forecast for Australia 2026, which represents:

- High housing demand and high housing supply

- Long-term housing shortages

- Continued government subsidies for first-home buyers

- Changing investor and owner-occupier behaviour

This combination is the reason why the trends in the Australian property market 2026 have steady momentum.

City-Level Insight: Where Growth Is Expected

The performance of the market in 2026 is going to be highly diverse in capital cities, which supports the necessity of location-specific analysis of property investment Australia.

- Perth is projected to record the highest growth nationally, with annual price increases forecast between 12-13% Given by population growth and economic expansion. For investors seeking guidance, working with a buyers agnet perth can give investors who are looking for advice strategic insight into suburbs that are performing well.

- Brisbane and Darwin are also expected to experience a high growth of over 10% and will be aided by the relatively low cost.

- Adelaide will experience relatively average growth of mid-single digits; this implies that the market fundamentals are improving.

- Sydney and Melbourne are likely to experience slower growth of about 5-7%, which is due to high entry prices and loan limits.

This difference indicates the importance of professional market analysis in the assessment of the best cities to invest in property Australia 2026.

Affordability and Market Drivers for 2026

Affordability is also one of the largest issues that is informing the Australian housing market outlook. Shifts in the cash rate of the Reserve Bank of Australia and the tightening of the lending conditions have lowered the borrowing capacities of most buyers.

In spite of this, the demand is robust because of:

- Stable employment levels

- Gradual wage growth

- Continued migration

- Lack of housing opportunities

As a result, most buyers are considering outer-suburban and regional expansion areas in pursuit of enhanced values in the property affordability Australia model.

The initiatives by the government, like the disseminated 5% Deposit Scheme, are also contributing to the growth of competition between eligibility price lines.

Rental market Trends and investment signals

The demand and supply in the rental markets are believed to be tight in the year 2026, which will further boost the property investors in Australia. High occupancy rates and the lack of supply have raised the rent to record-high levels in most areas.

Favourable rental terms have sustained real estate that has the potential to become a good rental yield. Thus, income-earning assets remain appealing in diversified investment portfolios.

This economic climate supports more strategic thinking to invest in the best real estate investment in Australia, to balance between capital expansion and long-term cash flow.

Risk and Headwinds: What Buyers Should Watch

Though the overall market mood is optimistic, there are a number of risks that might affect the trend in property prices Australia:

- Affordability pressures may limit buyer capacity in premium suburbs.

- Interest rate uncertainty remains a major economic variable.

- Regional market divergence may create uneven performance outcomes.

These risks are important to understand in case professionals are interested in long-term property investment strategies.

What This Means for Australian Buyers and Investors

The Australian property market outlook 2026 is an indicator of a strong but picky market. Key implications include the following:

- Continued national house prices growth supported by fundamentals

- Increased regional/outer-metro market significance.

- Strong rental market keeping investor confidence

- Growing professional requirements of professional data-driven decision-making

To buyers and investors, a mix of trustworthy market research with individualised recommendations is still the key to successful navigation in property market trends.

Conclusions: Navigation 2026 with Insight and Strategy

The housing market in Australia in 2026 is both a chance and a challenge. Although the national forecasts suggest constant growth and strengths of the rental, regional variations and affordability issues demand planning.

Whether you are in the market as a first-time buyer or you are looking to add to your investment portfolio, knowing where property prices are headed next will help you make decisions that will be future-orientated.

Keep in touch with Buyer Insight to keep up with what is going on in the market and to get the comments of experts.

Follow us on Instagram.

Follow us on Facebook.

Connect on LinkedIn.

Contact on: 61 468 444 478

Are you ready to build your property strategy? Get a free consultation with our professional team and get a personal plan on achieving your 2026 property goals.